论文

由实证检验到理论猜想:证券价格与价值偏离的时变路径及其生成机理

摘要

对证券价格与证券价值关系问题的回答关乎现代金融理论的延展,影响着资本市场实践操作准则的甄选。建立在对传统金融理论和行为金融理论关于证券价格与价值关系问题分歧的基础上,本文依据剩余收益模型测度了证券价格与价值的偏离,描绘了证券价格与价值偏离的时变路径,并实证检验了该时变路径的成因,最终从理论猜想角度阐释了证券价格与价值偏离时变路径的生成机理。研究结果显示,证券价格与价值偏离的时变路径具有明显的循环往复的非线性结构,原因在于该时变路径主要由周期成分和外生冲击成分两部分构成,其中周期成分决定了时变路径的基本结构,外生冲击成分决定了时变路径的具体结构。金融市场会延续宏观经济系统的一般性特征和现象,进而对宏观经济系统的特征和现象形成一定程度的“映射”:金融市场及其微观主体依据经济周期和证券价格与价值偏离做出的行为选择促成了证券价格与价值时变路径的周期成分,而影响宏观经济系统和金融市场的宏微观冲击是证券价格与价值时变路径外生冲击成分的生成源,这是关于证券价格与价值偏离时变路径生成机理的理论猜想。该理论猜想是以实证检验为基础进行的理论挖掘,缺少对生成机理微观基础的数据检验和论证。从微观视角考察上市公司和投资者在经济周期和证券价格与价值偏离不同状态下的行为选择活动,将是未来的研究方向。

参考文献 查看全部 ↓

检索正文关键字

论文目录

- 引言

- 1 文献综述

- 2 证券价格与价值偏离的计算方法及数据

-

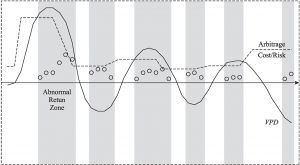

3 证券价格与价值偏离的时变路径

- 3.1 证券价格与价值偏离的变动路径

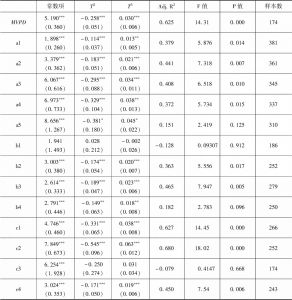

- 3.2 证券价格与价值偏离时变路径的成因

- 4 证券价格与价值偏离时变路径的生成机理

- 5 结论

论文图片/图表

查看更多>>>