论文

美国法学院开设财务会计课程的经验与借鉴

摘要

为培养复合型法学人才,法学院自己开设会计课极为必要,因为财务会计信息的法律本质是法律事实,不仅优秀的商业律师必须掌握基础会计知识,就连法官也需要具备一定财会素养,财务会计知识更是深刻理解公司法、金融法等商法的基础之一。我国法学院现有的会计法专业课、会计学实验班、会计学公选课等三种模式,皆不能完全满足法科人才培养需要。美国法学院经验非常值得借鉴:几乎所有法学院都开设了由法学教授主讲的会计课,除基础会计课外,还有会计与商法交叉领域的专业课程,目标明确为律师从事法律实践必备的财会知识。笔者认为,我国法学院应开设“给法科生的会计课”,并应将之作为民商法、经济法专业的必修课,教学目标以律师服务企业为导向,教学内容围绕企业财务会计报告及会计程序展开,从而培养更能满足商业与法律实践需要的复合型人才。

作者

冯兴俊 ,女,贵州贵阳人,法学博士,中南财经政法大学法学院副教授。

检索正文关键字

论文目录

-

一 法学院自己开设会计专业课程已刻不容缓

- (一)财务会计信息的法律本质是法律事实

- (二)优秀的商业律师必须掌握基础会计知识

- (三)法官等非律师职业同样需要具备一定财会素养

- (四)加深对公司法等商法的理解必须以财会知识为基础

-

二 美国法学院的会计课程值得借鉴

- (一)国内既有会计类课程模式述评

- 1.会计法专业课模式

- 2.会计学实验班模式

- 3.会计学公选课模式

- (二)美国法学院会计课的经验

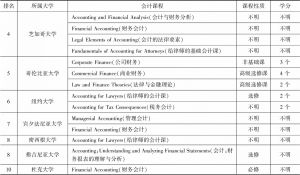

- 1.几乎所有美国法学院都开设了会计类课程

- 2.法学院的财会类课程分为两个层次

- 3.法学院的会计课教学目标非常明确

- 4.相关课程由法学院教师讲授

- (一)国内既有会计类课程模式述评

-

三 对我国法学院开设会计课程的建议

- (一)“给法科生的会计课”应成为民商法、经济法专业的必修课

- (二)教学目标应以律师服务企业为导向

- (三)教学内容围绕企业财务会计报告及会计程序展开

- (四)应由法学院开课、法学教师授课

论文图片/图表

相关文献

查看更多>>>