摘要

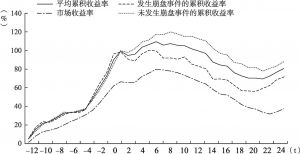

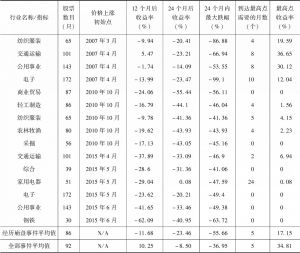

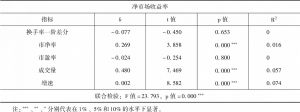

2014年,Fama提出了非理性泡沫理论,即股票或投资组合的价格大幅度上涨,并不意味着其在未来一定具有异常低的平均收益率。为了验证Fama非理性泡沫理论在中国股票市场的适用性,本文选取2000~2019年中国行业相关数据对Fama非理性泡沫进行检验,同时选择8个特征变量对未来股票发生崩盘事件的可能性以及股票未来收益率进行预测。研究结果表明,Fama的观点是正确的,未来的收益率在很大程度上是不可预测的,行业投资组合的价格大幅上涨并不意味着未来异常低的收益率,而预示着股票未来崩盘事件发生的可能性会大幅增加。同时,与价格上涨后股票未发生崩盘的事件相比,发生崩盘事件对应的行业股票往往具有较小的涨跌幅、较高的换手率、较大的成交量、较低的市净率、较低的市盈率以及较快的收益率下降速度。此外,利用这些变量可以实现对未来收益率的联合预测,从而帮助投资者在一定程度上有效地避免股票崩盘。

作者

张筱婉 (1984- ),女,吉林大学商学院博士研究生,主要研究方向为宏观经济计量。

方毅 (1976- ),男,吉林大学数量经济研究中心、吉林大学商学院教授,博士生导师,主要研究方向为金融数量分析。

牛慧 (1997- ),女,吉林大学商学院硕士研究生,主要研究方向为金融数量分析。

- 陈信元,张田余,陈冬华.2001.预期股票收益的横截面多因素分析:来自中国证券市场的经验证据[J].金融研究,(6):22-35.

- 方毅,孟佶贤,曲俊雪.2019.基于市场异象的多因子定价模型比较研究[J].数量经济研究,10 (1):82-96.

- 王茵田,朱英姿.2011.中国股票市场风险溢价研究[J].金融研究,(7):152-166.

- 徐德财,初梓健,周津宇.2019.由实证检验到理论猜想:证券价格与价值偏离的时变路径及其生成机理[J].数量经济研究,(3):74-99.

- 张矢的,高明宇,吴斌.2014.未充分分散投资下的资本资产定价模型:基于中国A股市场的实证检验[J].管理评论,26 (10):24-37.

- Barberis,N.,R.Greenwood,L.Jin,,A.Shleifer. 2018. Extrapolation and Bubbles[J]. Journal of Financial Economics,129 (2):203-227.

- Benjamini,Y.,Y.Hochberg. 1995. Controlling the False Discovery Rate:A Practical and Powerful Approach to Multiple Testing[J]. Journal of the Royal Statistical Society:Series B,57:289-300.

- Bonferroni,C.E. 1936. Teoria Statistica Delle Classi e Calcolo Delle Probabilità[J]. Pubblicazioni del R Istituto Superiore di Scienze Economiche e Commerciali di Firenze,8:3-62

- Campbell,J.Y.,M.Lettau,B.G.Malkiel,Y.Xu. 2001. Have Individual Stocks Become More Volatile?—An Empirical Exploration of Idiosyncratic Risk[J]. Journal of Finance,56 (1):1-43.

- Dunn,O.J. 1959. Estimation of the Medians for Dependent Variables[J]. Annals of Mathematical Statistics,30 (1):192-197.

- Estrada,J.,A.P.Serra. 2005. Risk and Return in Emerging Markets:Family Matters[J]. Journal of Multinational Financial Management,15 (3):257-272.

- Fama,E.F.,K.R.French. 1992. The Cross-section of Expected Stock Returns[J]. The Journal of Finance,47 (2):427-465.

- Fama,E.F.,K.R.French. 1993. Common Risk Factors in the Returns on Stocks and Bonds[J]. Journal of Financial Economics,33 (1):3-56.

- Goetzmann,W.N. 2016. Bubble Investing:Learning from History[R]. NBER Working Papers,3:149-168.

- Hong,H.,J.C.Stein. 2007. Disagreement and the Stock Market[J]. Journal of Economic Perspectives,21 (2):109-128.

- Huang,J.,J.Wang. 2009. Liquidity and Market Crashes[J]. Review of Financial Studies,22 (7):2607-2643.

- Jegadeesh,N.,S.Titman. 1993. Returns to Buying Winners and Selling Losers:Implications for Stock Market Efficiency[J]. Journal of Finance,48 (1):65-91.

- Mackay,C. 1841. Extraordinary Popular Delusions and the Madness Of Crowds[M]. Farrar,Straus and Giroux.

- Ofek,E.,M.Richardson. 2003. Dotcom Mania:The Rise and Fall of Internet Stock Prices[J]. Journal of Finance,58 (3):1113-1137.

- Shiller,R. 2000. Irrational Exuberance[M]. Princeton University Press.

- 陈信元,张田余,陈冬华.2001.预期股票收益的横截面多因素分析:来自中国证券市场的经验证据[J].金融研究,(6):22-35.

- 方毅,孟佶贤,曲俊雪.2019.基于市场异象的多因子定价模型比较研究[J].数量经济研究,10 (1):82-96.

- 王茵田,朱英姿.2011.中国股票市场风险溢价研究[J].金融研究,(7):152-166.

- 徐德财,初梓健,周津宇.2019.由实证检验到理论猜想:证券价格与价值偏离的时变路径及其生成机理[J].数量经济研究,(3):74-99.

- 张矢的,高明宇,吴斌.2014.未充分分散投资下的资本资产定价模型:基于中国A股市场的实证检验[J].管理评论,26 (10):24-37.

- Barberis,N.,R.Greenwood,L.Jin,,A.Shleifer. 2018. Extrapolation and Bubbles[J]. Journal of Financial Economics,129 (2):203-227.

- Benjamini,Y.,Y.Hochberg. 1995. Controlling the False Discovery Rate:A Practical and Powerful Approach to Multiple Testing[J]. Journal of the Royal Statistical Society:Series B,57:289-300.

- Bonferroni,C.E. 1936. Teoria Statistica Delle Classi e Calcolo Delle Probabilità[J]. Pubblicazioni del R Istituto Superiore di Scienze Economiche e Commerciali di Firenze,8:3-62

- Campbell,J.Y.,M.Lettau,B.G.Malkiel,Y.Xu. 2001. Have Individual Stocks Become More Volatile?—An Empirical Exploration of Idiosyncratic Risk[J]. Journal of Finance,56 (1):1-43.

- Dunn,O.J. 1959. Estimation of the Medians for Dependent Variables[J]. Annals of Mathematical Statistics,30 (1):192-197.

- Estrada,J.,A.P.Serra. 2005. Risk and Return in Emerging Markets:Family Matters[J]. Journal of Multinational Financial Management,15 (3):257-272.

- Fama,E.F.,K.R.French. 1992. The Cross-section of Expected Stock Returns[J]. The Journal of Finance,47 (2):427-465.

- Fama,E.F.,K.R.French. 1993. Common Risk Factors in the Returns on Stocks and Bonds[J]. Journal of Financial Economics,33 (1):3-56.

- Goetzmann,W.N. 2016. Bubble Investing:Learning from History[R]. NBER Working Papers,3:149-168.

- Hong,H.,J.C.Stein. 2007. Disagreement and the Stock Market[J]. Journal of Economic Perspectives,21 (2):109-128.

- Huang,J.,J.Wang. 2009. Liquidity and Market Crashes[J]. Review of Financial Studies,22 (7):2607-2643.

- Jegadeesh,N.,S.Titman. 1993. Returns to Buying Winners and Selling Losers:Implications for Stock Market Efficiency[J]. Journal of Finance,48 (1):65-91.

- Mackay,C. 1841. Extraordinary Popular Delusions and the Madness Of Crowds[M]. Farrar,Straus and Giroux.

- Ofek,E.,M.Richardson. 2003. Dotcom Mania:The Rise and Fall of Internet Stock Prices[J]. Journal of Finance,58 (3):1113-1137.

- Shiller,R. 2000. Irrational Exuberance[M]. Princeton University Press.