章节

中国非金融企业的金融投资行为影响机制研究

摘要

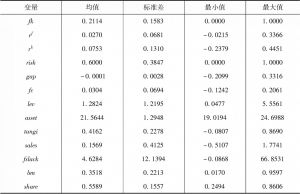

本文构建了中国非金融企业的金融投资行为影响机制理论模型。我们基于微观企业面对实业投资和金融投资两大类资产的投资组合选择背景,拓展已有研究关于微观企业投资组合模型中金融投资无风险的假设,同时考虑金融投资风险和固定投资风险,推演出与现实情况更加贴近的理论模型。本文证明,拓展模型与传统模型的机制存在本质区别。基于中国A股非金融上市公司面板数据的实证结果表明,中国非金融企业金融投资行为的显著驱动因素是固定资产投资的风险占比,而不是金融资产与固定资产的投资收益率缺口。

检索正文关键字

章节目录

- 一 引言

- 二 理论模型的对比与竞争

- 三 基于理论模型的实证假说及变量说明

-

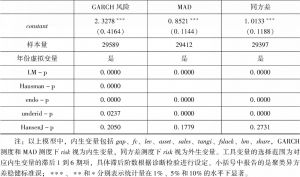

四 实证分析

- (一)基础模型的估计结果

- (二)稳健性分析

- 五 结论与建议

章节图片/图表

相关文献

查看更多>>>