- 分享

-

收藏(0)

查看图表上下文

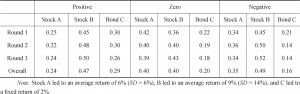

Figure 3 Participants’ Average Portfolios Represented by the Investments in Stock B and Bond C of the Three Conditions of Experiment No.1,Compared With the Average Predictions of the Basic Reinforcement (BR) Learning Model and the Risk-return-covariance (RRC) Model. The x-axes Represent the 90 Periods of the Whole Experiment Partitioned Into Nine Blocks of 10 Periods Each.

资源编号:1586030

图表出处:Frontiers in Economic and Management Research (Volume 7) 出处详情

关键词:

所属学科:国民经济计划学

图表描述:

图表规格:jpg

免费查看原图 查看全文

社会科学文献出版社版权所有

同文图表查看更多>

-

图表出处:Frontiers in Economic and Management Research (Volume 7)

-

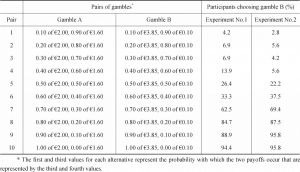

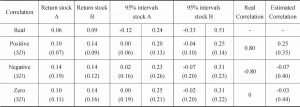

Table 3 Investments in the Three Assets Across the Three Correlation Conditions of Experiment No.1

图表出处:Frontiers in Economic and Management Research (Volume 7)

-

图表出处:Frontiers in Economic and Management Research (Volume 7)

-

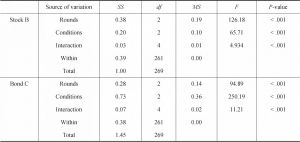

Table 8 Two Factor Repeated Measurement ANOVA of Experiment No.2

图表出处:Frontiers in Economic and Management Research (Volume 7)

-

Table 10 Participants’ Estimations of the Two Stock Returns and Variability in Experiment No.2

图表出处:Frontiers in Economic and Management Research (Volume 7)