论文

企业社会责任信息披露与股价同步性:“价值创造”还是“自利工具”?

摘要

企业披露社会责任信息究竟是出于股东的“价值创造”动机,还是出于管理层的“自利工具”动机,一直是企业社会责任研究中富有争议的话题。以2009~2017年中国A股上市公司为样本,本文考察了企业社会责任信息披露对股价同步性的影响以及传导路径。研究发现,企业披露社会责任信息与股价同步性呈正相关关系,而且信息透明度在企业社会责任信息披露对股价同步性的影响中发挥中介作用。这表明企业社会责任信息披露并没有使企业股票被合理定价,反而干扰了投资者的判断,导致股价同步性提高,支持了企业披露社会责任信息的“自利工具”动机。进一步基于产权性质进行异质性分析发现,相较于国有企业,非国有企业的社会责任信息披露对股价同步性的提升作用更加突出。

关键词

参考文献 查看全部 ↓

检索正文关键字

论文目录

- 一、引言

-

二、文献综述与研究假设

- (一)文献综述

- 1.股价同步性

- 2.企业社会责任(信息披露)

- (二)研究假设

- (一)文献综述

-

三、研究设计

- (一)样本来源

- (二)实证模型

- (三)变量定义

- (四)描述性统计

-

四、实证分析

- (一)回归分析

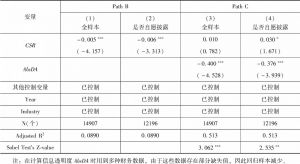

- (二)路径研究:信息透明度的中介作用

- 五、拓展分析:产权性质的影响

-

六、稳健性检验

- (一)倾向评分匹配

- (二)变量替换

- 七、结论与启示

论文图片/图表

查看更多>>>